Author: Solomon Abudarham | Leader for Trade and Partnership Development

After the declaration of pandemic in March 2020 by the World Health Organization (WHO), the situation plunged governments, companies, and markets into uncertainty. This created a breakdown in financial expectations and pushed economies and businesses around the world to seek ways to adapt. After seven months, the consumer confidence remains expectant about reactivation measures and policies.

However, despite a subsequent economic reactivation, Latin America and the Caribbean has been one of the most affected regions. In the words of Dr. Arun Singh, Dun & Bradstreet Global Chief Economist: “The region is lagging behind others despite signs of gradual recovery in Brazil and Mexico from the nadir of the Q2 coronavirus-induced shock. Economic activity will accelerate unevenly throughout the region to the end of 2020 as trade, investment and remittances are severely reduced.”

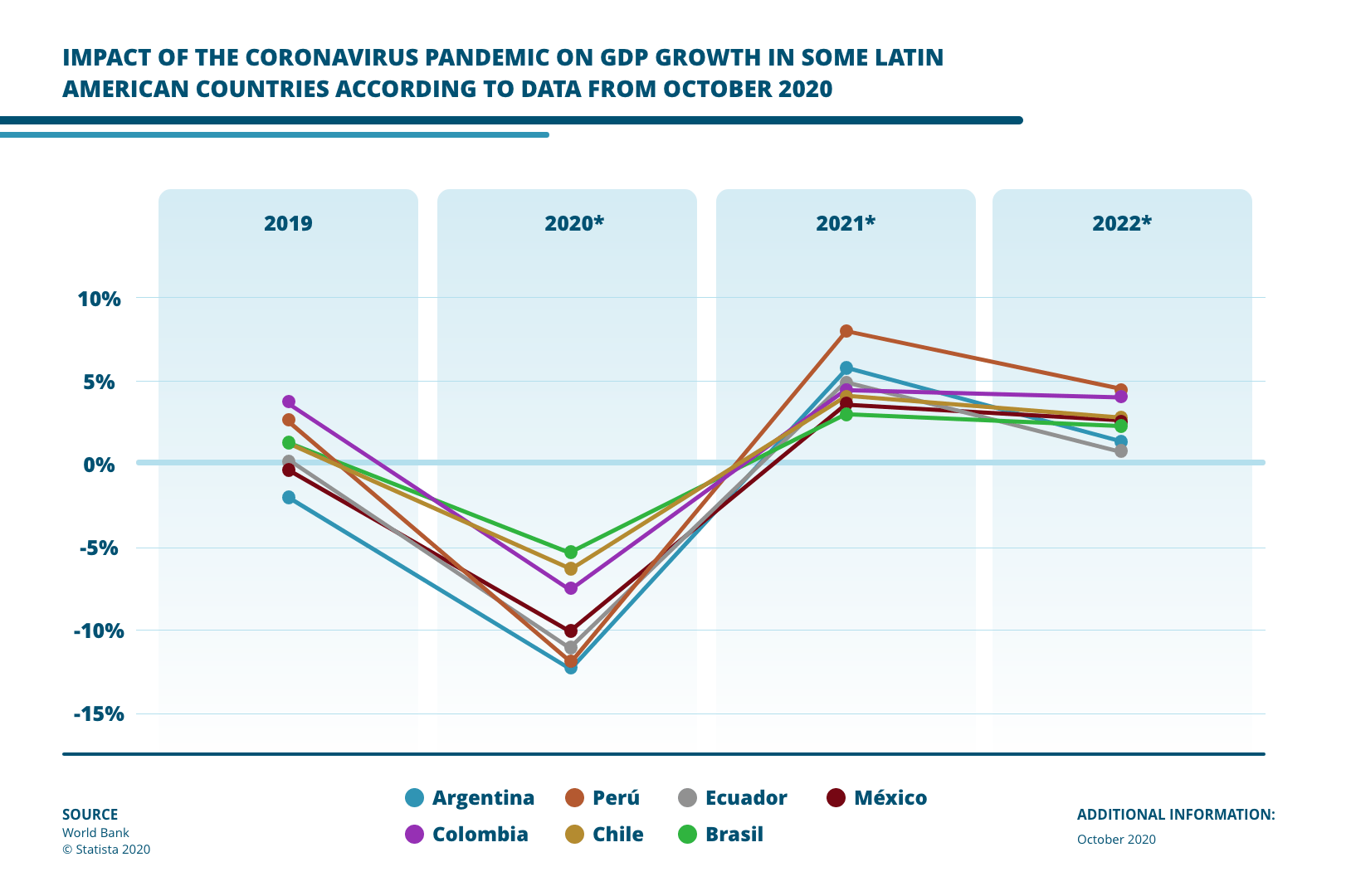

Source: World Bank

With the impact still evolving, there are risk factors to consider, which can be key to the development or wear of a company during the global crisis that we are experiencing. The resumption of forced closures and the persistent cases of COVID-19 further prolong the recovery and extend the regional and global economic recession. In addition to this, the new waves of contagion in Europe make the markets require a new round of trade and movement blockades in that continent. In addition, the increase in the delinquency rates of the securities backed in North America could cause bankruptcies and consequences in the medium and long term for multinational investors.

Faced with a scenario like this, credit becomes an ideal tool for companies to meet their service demands and face present and future challenges in the times of COVID-19. The precision of the amounts to be granted, terms and detailed knowledge of the entity, must be deeply analyzed so that this option fulfills its function and allows solving setbacks in the medium term.

In 2019, credit in Latin America proved to be a dynamic possibility, presenting a positive performance despite the general low economic growth in the region. This dynamism helped international trade and private investment, both local and external. The Latin American Federation of Banks (Felaban), considered that its entities in the region have shown a resilient tendency to adapt to adverse conditions, in addition to maintaining good profitability indicators at the international level. All the above, regardless periods of low economic growth and that entrepreneurs take a more careful stance with their investments.

Although the emergence of COVID-19 changed the global landscape, credit remains a tangible option to cope with the decline in percentages and flows in supply chains. Companies in all industries have had to develop extraordinary strategies, including the decisive management of customer loans, as in some cases in the field of transportation.

Although the emergence of COVID-19 changed the global landscape, credit remains a tangible option to cope with the decline in percentages and flows in supply chains. Companies in all industries must develop extraordinary strategies, including the decisive management of customer loans, as in some cases in the field of transportation.

In this regard, the general director of TDR Soluciones Logísticas, commented that they had the need to establish a crisis management committee, in charge of outlining the strategies to take care of the cash, this to provide the company with “oxygen” and generate more confidence in people with a “financially healthy” company. Measures such as being careful during the process of granting loans, analyzing and knowing in detail your collection funds and maintaining a frank dialogue with customers and suppliers about expectations, capacities and specific payment dates, are the column of credit as an alternative.

After the WHO declared the pandemic in March, uncertainty dipped governments, companies, and markets. This made consumer confidence remain hesitant and expectant. Given this, and an uneven economic activation in América Latina during 2020, credit becomes an ideal tool for companies to continue attending their demands and face current and future challenges. This possibility proved to be a dynamic option in LATAM during 2019 despite the low economic growth.

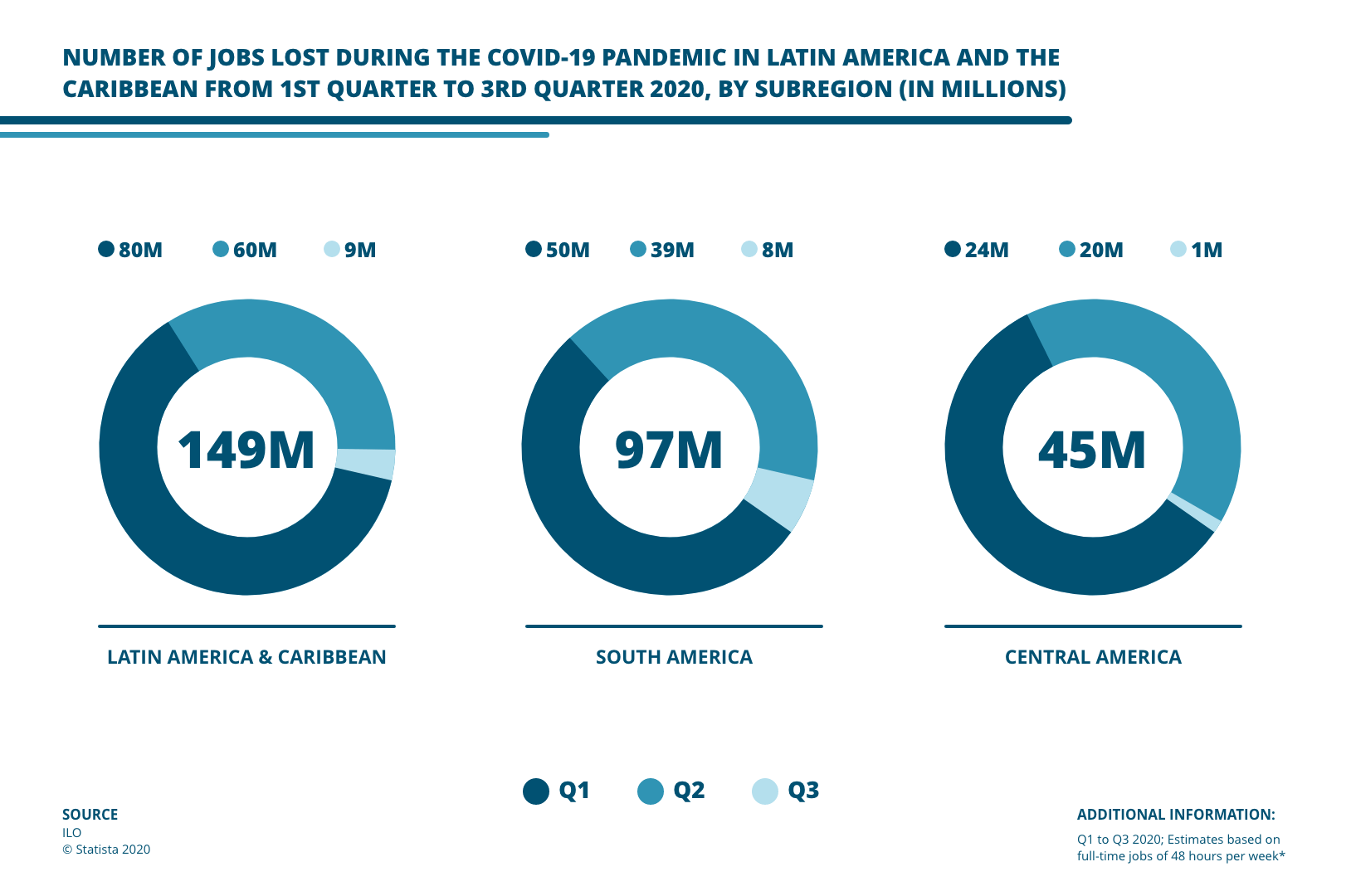

Source: International Labour Organization

What measures do companies have had to take to reduce risks? Many have created different strategies such as crisis management committees, made exhaustive reviews of collections funds and detailed analysis to grant credit. Incorporate an adequate balance of risks, establish precise credit limits and monitor the risk of the portfolio of each area. In CIAL Dun & Bradstreet we work in solutions aligned to companies’ most pressing needs, such as CIAL 360 Credit, which can help you automate credit decisions based on the most updated and reliable information.

Extending low-risk credit

The new economic reality has generated more active measures to mitigate credit risks in the supply chains of each company. Some of the options to consider are:

- Incorporate an appropriate balance of risks: a prolonged period of economic prosperity and minimal bankruptcies may have influenced the focus of day-to-day credit policy, allowing more risk in the portfolio than would be prudent in an environment of slow growth or a recessive economy. To reassess the credit policy of a company it is necessary to recalibrate the risk profile of the portfolio of new and existing clients.

- Establish adequate credit limits: This opportunity should be taken to realign credit limits and learn about the credit exposure you have for the entire global corporate hierarchy of that client. In the same way, it is advisable to adjust the credit limits (increasing or reducing them) according to the assessment of the individual risk of the client.

- Establish appropriate terms: Assessing the potential risk of each new opportunity or customer renewal will help realign credit terms based on the probability that the customer will pay on time and within those terms.

- Portfolio risk monitoring: Perhaps more urgently, consider implementing credit risk monitoring for the entire global portfolio to identify weaknesses that could lead losses from bad debts or potential bankruptcies.

Given the new economic situation that the region and the whole world is facing, the most appropriate thing is to have the relevant information and make the best decisions with a proactive approach that allows to anticipate risks, understand opportunities and make of the credit a possibility for a company’s supply chains to follow their cycles.